LOAN & MORTGAGES GUIDE

Mortgage Education & Smart Borrowing | State Global

Loans & Mortgages Made Clear

Whether purchasing a home, refinancing, or consolidating debt, understanding how loans work helps you make confident financial decisions.

At State Global, we simplify lending so you can borrow responsibly and strategically.

Mortgage Basics Explained

A mortgage is a loan used to purchase or refinance property. The lender provides funds, and the borrower agrees to repay over time with interest.

Key Mortgage Components:

Principal

The original amount borrowed.

Interest

The cost of borrowing money.

Term

The length of the loan (commonly 15 or 30 years).

Down Payment

The upfront amount paid toward the purchase price.

Escrow

Funds set aside for property taxes and insurance.

What Determines Your Mortgage Rate?

Credit score

Debt-to-income ratio (DTI)

Loan amount

Loan term

Market interest rates

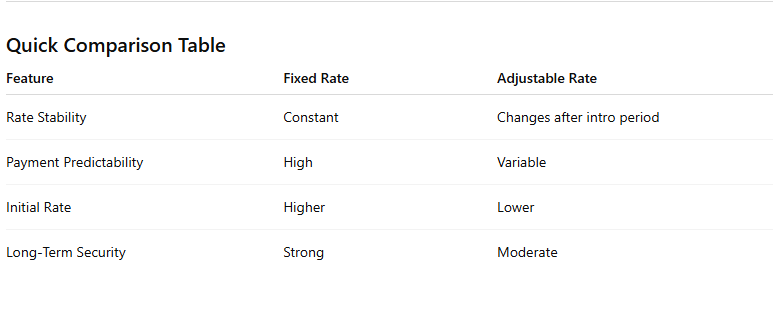

Fixed vs. Adjustable Rate Loans

Choosing the right loan type is critical.

Fixed-Rate Mortgage

✔ Interest rate remains the same

✔ Predictable monthly payments

✔ Ideal for long-term homeowners

Best For: Borrowers who want stability and consistent budgeting.

Adjustable-Rate Mortgage (ARM)

✔ Lower initial interest rate

✔ Rate adjusts after introductory period

✔ Payments may increase or decrease

Best For: Short-term homeowners or those expecting income growth.

Loan Pre-Qualification Guide

Pre-qualification gives you an estimate of how much you may be eligible to borrow.

Review Your Credit Profile

Higher credit scores generally qualify for better rates.

Calculate Debt-to-Income Ratio (DTI)

DTI = Total Monthly Debt ÷ Gross Monthly Income

Ideal: Below 43%

Gather Documentation

Proof of income

Employment verification

Bank statements

Tax returns

Receive Pre-Qualification Letter

This strengthens your offer when buying a home.

Debt Consolidation Strategies

Debt consolidation combines multiple debts into one manageable payment.

Benefits of Consolidation

✔ Lower overall interest rate

✔ Simplified monthly payments

✔ Potential credit score improvement

✔ Faster debt payoff

Common Consolidation Options

Personal consolidation loan

Home equity loan

Balance transfer credit card

Mortgage refinance

When Consolidation Makes Sense

High-interest credit card balances

Multiple payment due dates

Difficulty tracking debt

Example Scenario

Original Debt:

$15,000 at 22% interest

Consolidation Loan:

$15,000 at 10% interest

Potential Outcome:

Lower monthly payment and reduced total interest cost over time.

-

Typically, 620+ for conventional loans (varies by program).

-

Ranges from 3%–20% depending on loan type.

-

Soft inquiries generally do not; formal applications may.