UNDERSTANDING CREDIT, APR & RESPONSIBLE BORROWING | State Global

Credit & Borrowing Made Simple

Credit plays a central role in financial stability. Whether applying for a mortgage, auto loan, or credit card, your credit profile influences approval decisions and interest rates.

At State Global, we believe informed borrowers make stronger financial decisions.

How Credit Scores Work

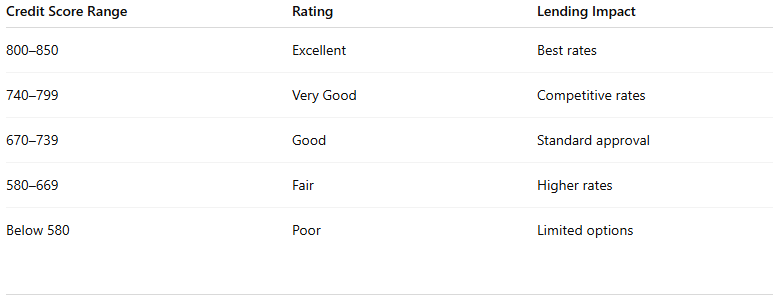

A credit score is a numerical representation of your creditworthiness. It typically ranges from 300 to 850.

What Impacts Your Credit Score?

Payment History (35%)

On-time payments improve your score

Late payments significantly reduce it

Credit Utilization (30%)

How much of your available credit you use

Ideal: Keep balances below 30% of your limit

Length of Credit History (15%)

Longer credit history increases stability

Credit Mix (10%)

A mix of credit cards, auto loans, mortgages

New Credit Inquiries (10%)

Multiple hard inquiries in a short period can lower your score

Improving Your Credit Profile

Improving your credit takes discipline and consistency.

✔ Make All Payments on Time

Payment history is the largest factor.

✔ Lower Credit Utilization

Pay down balances before statement closing dates.

✔ Avoid Opening Multiple Accounts at Once

Too many new accounts can signal risk.

✔ Keep Older Accounts Open

Length of history matters.

✔ Review Your Credit Report Annually

Check for errors and dispute inaccuracies.

Pro Tip: Even small balance reductions can quickly improve utilization ratios.

Understanding APR vs. Interest Rate

Many borrowers confuse these two terms.

Interest Rate

The percentage charged on borrowed money.

APR (Annual Percentage Rate)

The total annual cost of borrowing, including:

Interest

Certain fees

Additional lender charges

APR provides a more accurate comparison between loan offers.

Example:

Loan A:

6% interest rate

6.2% APR

Loan B:

6% interest rate

6.8% APR

Loan A is less expensive overall due to lower fees.

Responsible Use of Credit Cards

Credit cards can be powerful financial tools when used correctly.

Best Practices:

✔ Pay your balance in full each month

✔ Keep utilization below 30%

✔ Avoid cash advances

✔ Set payment reminders

✔ Monitor transactions regularly

Benefits of Responsible Use:

Builds credit history

Earns rewards

Provides fraud protection

Improves loan eligibility

Risks of Misuse:

High interest accumulation

Increased debt burden

Credit score damage

-

Description text goes hereA score above 670 is generally considered good.

-

Description text Positive changes may appear within 30–90 days, depending on actions taken. Goes here

-

Soft inquiries do not affect your score. Hard inquiries may.